- Strong commitment to become a digital ‘main bank’ by allocating more than 50% of its capital to growth, productivity and digital transformation.

- Digital NPS increased 32% YoY as a result of advanced usage of data analytics and personalisation

- Full suite of digital capabilities and enhanced propositions through strategic partnerships

Standard Chartered Bank Hong Kong (StanChart HK) has taken the lead in providing integrated digital banking services in Hong Kong. The bank invested heavily on improving digital banking experience to deliver a seamless omni-channel experience, particularly its digital capabilities and overall customer experience.

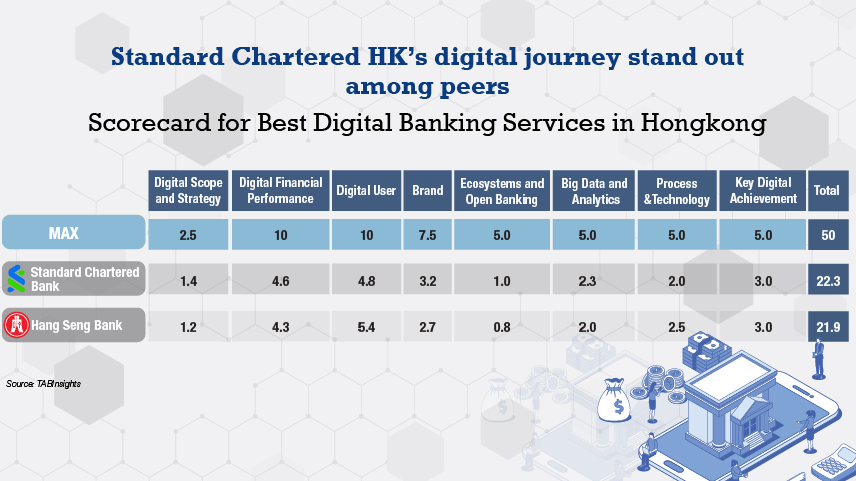

The bank was recognised for Best Digital Banking Services in Hong Kong in the Excellence in International Retail Financial Services Awards Programme 2022

Digital Scope and Strategy

Stanchart HK successfully delivered its three strategic priorities: scale growth in affluent and wealth management, drive individual segment with digital, and differentiate with client experience, supporting the community during these unprecedented times.

The core tenet of its digital wealth strategy is to compete better than traditional peers and digital-only banks by delivering a combination of human expertise and digital. The rollout of ‘My RM’ combines those elements, enabling customers to continuously interact and execute transactions with relationship managers (RMs) and advisors when it comes to more complex products such as life insurance or structured products.

Growing the bank’s frontline capacity and upskilling RMs and specialists, the Standard Chartered-INSEAD Wealth Academy was launched in 2021 which strengthened the bank’s strategic agenda to grow its affluent banking business.

Stanchart HK allocates more than 50% of its capital to growth, productivity and digital transformation. While many digital capabilities were already in place by end of 2019 such as digital deposits, digital onboarding, digital foreign exchange (FX), mutual funds and brokerage, the bank enhanced those capabilities in 2020. In 2021, the bank further extended investment account opening for securities and funds to its mobile app and expanded its online equities platform to include the US market. This enabled clients to grasp growth opportunities across HK, China and US securities markets with a single account.

Stanchart HK launched one of the city's first cardless cash withdrawals with QR code in 2018 and provides various digital banking services such as personalised wealth management tool, ‘My RM’, instant account opening, virtual onboarding for insurance and instant interbank transfer.

Digital Financial Performance

To drive sales, the bank is utilising the most appropriate tools in acquisition. In 2021, there has been all-rounded growth in digital sales, revenue and online channel share. Revenue generated from digital sales increased by 40% in 2021, with major contributors from time deposits, unit trusts, equities and credit card instalments. In particular, the share of digital sales of unit trusts increased to 77% in 2021.

The bank posted a 27% YoY increase in digital sales of retail banking products which increase the contribution to 51%; in particular, the share of digital sales of unit trusts increased to 77% in 2021. This performance elevated Stanchart HK becoming the top digital sales play compared to its closest peers. It also posted a 36% YoY increase in digital payments and transaction.

Overall industry revenue growth in retail financial services in 2021 reflects the ongoing operating challenges banks face in this market. Industry revenue in retail declined by 7% YoY. While Stanchart HK bank was in line with industry averages, Hang Seng Bank performed slightly better with retail revenue declining by 6% YoY. Bank of East Asia’s retail revenue declined by 12% YoY.

Digital Users and Brand

About 75% of banking services at Stanchart HKwere conducted through digital channels, and the number of customers using mobile banking services grew by 21% YoY in 2021. The bank has full digital onboarding capabilities across current accounts, personal loans and credit cards. More than 80% of credit cards are onboarded and processed digitally and 80% of all services requests in retail financial services have been automated.

Hong Kong has a high digital banking adoption rate, with more than 50% of customers conducting their banking needs via desktop or mobile banking prior to the pandemic, and many customers have shifted further their everyday banking from offline to online to cover their banking needs since 2020. Most first-tier banks established digital electronic know your customer (eKYC) onboarding prior to the outbreak.

Standard Chartered Bank posted strong growth in digital users with a digital active rate of over 50% over a three-month rolling base, 10% higher than peer average in Hong Kong. It was however Hang Seng Bank which achieved higher digital active rates and stronger mobile growth numbers.

Stanchart HK’s net promoter score (NPS) in mobile banking saw the biggest gains in 2021 increasing by 12% in 2021, taking a comprehensive lead to Hang Seng Bank. It also outperformed in growing its deposit base compared to Hang Seng Bank whose retail deposit base declined by 1% YoY.

Ecosystem and Open Banking

Stanchart HK aims to respond faster to the rapidly changing client behaviour and market landscape in Hong Kong and capture growth opportunities. To do so, the bank is on a journey to expand its agile working mode across more teams and business units on top of setting up dedicated agile squads to focus on enhancing specific workflows and processes. More than 150 agile squads in the past two years saved more than 778,000 hours of client waiting time per annum. At the same time, the shift to the public cloud doubled in 2021, making StanChart (HK) one of the leading banks in cloud migration in this market.

In addition, StanChart (HK) is leveraging application programming interfaces (APIs) to connect with different aggregators and key web platform for client acquisition. While the financial retail industry in Hong Kong has been struggling to obtain real benefits out of their API-based partnerships in the past, the bank created several successful API-based services in 2021 that provide a smoother and more seamless way for customers to be onboarded. One example is the strategic partnership with AlipayHK which has about three million clients on its platform. To attract a younger segment, it launched Q Credit card within the AlipayHK app in which consumers can apply, get approved and use the card within one mobile app. It is the first physical and virtual credit card brought by the collaboration between an electronic wallet (e-wallet) and a bank in Hong Kong, enabling instant approval with a credit limit and consumption rewards for immediate use. E-wallets attracted more than 4.5 million new users and 90,000 new merchants in Hong Kong by the end of 2021.

Hong Kong has been one of the most robust property markets in terms of demand and transaction volume around the world and digitisation is a key driver in property market modernisation. Banks aim to leverage its strong API capabilities to connect with brokers and developers to facilitate customers' home buying journey and deliver a seamless and simple mortgage experience. Standard Chartered, for instance, rolled out its mortgage APIs with key mortgage brokers in the industry, allowing customers to pick and choose their mortgage package in one go without going to a branch or filling in multiple mortgage enquiry forms across different financial institutions. StanChart (HK) also provides digital straight-through processing for loans on cards, which enables instant loan approval and disbursement through online channels. This comes on the heels of Hang Seng Bank which developed two first-in-the-market API-powered services, namely E-valuation and mortgage E-referral, and deployed these APIs real estate companies. Since its launch, the home-buying APIs reached cumulated usage of over 7 million times and facilitated more than a thousand mortgage applications with a high conversion rate.

Big data and analytics

The leading plays in data and analytics among commercial banks in the Hong Kong Market, Stanchart HK and Hang Seng Bank, have expanded their big data and analytics applications to all major areas including marketing (e.g. next best offers), forecasting (forex forecasting), and ML comprehension (audio) and conversation.

Standard Chartered provides customers investment insight and idea from a fund list which the bank developed based on its vast databases, called "People Like You" featuring popular fund choices in the unit trust investment transactions of our different client groups. Those personalised offers support in a substantial way the bank’s digital sales.

In the past two years, StanChart HK has strengthened its client engagement platform by improving the digital client experience and engagement. It enables the bank to understand better the entire customer journey from the first touch, to conversion and engagement of different client segments and provides personalised experience at scale with automated contents and offers.

At the same time, the bank is exploring how to leverage on Hong Kong’s upcoming commercial data interchange (CDI), which aims to facilitate a more efficient way to tap into different types of data that are segregated across different sectors and entities.

Process, Technology and key digital achievements

StanChart HK continues to invest in new tools and capabilities for RMs to provide wealth advisory services remotely. The bank added a deposit order taking function to better serve clients with deposit transaction requests and upgraded personalised investment ideas (PII) – an in-house tool which facilitates RMs in analysing clients’ investment portfolio. Based on house views, market insights and clients’ holdings, the tool can now assess clients’ portfolio fitness and populate PII. PII is enabled on MyRM and BlueJeans platforms, a video conferencing app for RMs to conduct portfolio review remotely with clients.

From 2020 to end of 2021, the bank has launched more than 50 initiatives for robotic process automation (RPA) in operations.

With digital-only banks having a competitive edge in particular on the mobile UI/UX and digital journey fulfilment, commercial banks have been devoting more IT resources to this area to close the gap.

All Comments