|

Asia Pacific banks to earn $824 billion from retail by 2020

Retail financial services rather than corporate banking and treasury income will comprise the growth area for commercial banks in Asia Pacific in the coming five years. Emerging markets particularly the Philippines will generate the strongest growth, while China will generate the highest income by 2020. October 15, 2015 | Research

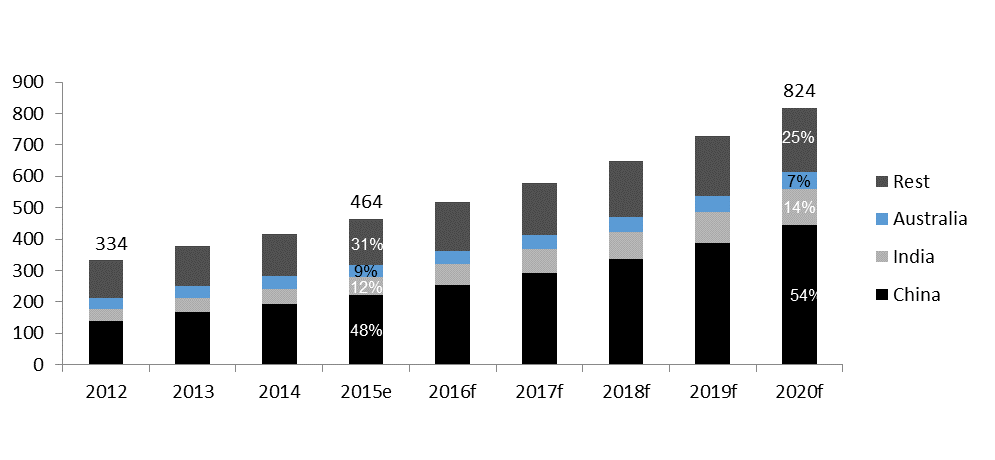

A large scale study conducted by Asian Banker Research on income generation in retail financial services in Asia Pacific found that commercial banks are expected to generate $464 billion in retail income by end of 2015, amid a growing shift away from thinning margins in corporate banking and volatile treasury income. The study took into consideration the outlook in gross income for retail financial services across 19 countries, including Australia, Brunei, Bangladesh, Cambodia, China, Taiwan, Japan, Vietnam, Sri Lanka, India, Hong Kong, Singapore, Indonesia, Thailand, Malaysia, Myanmar, Philippines, Korea and Vietnam. For the study retail banking income was defined as business from retail deposits, mortgages, credit cards/unsecured lending, wealth management and, wherever possible, SME banking. Commenting, Mobasher Zein Kazmi, head of research at The Asian Banker said “The ability to generate gross income in any given market is regarded as a key indicator of wallet share and a determinant of a bank’s bench strength in retail financial services. For the first time Asian Banker Research has ascertained the income potential in retail financial service markets across the Asia Pacific, and identified the top players.” Fig. 1: China expected to contribute the highest increase in income from retail financial services Retail Financial Services Income by Commercial Banks in Asia Pacific

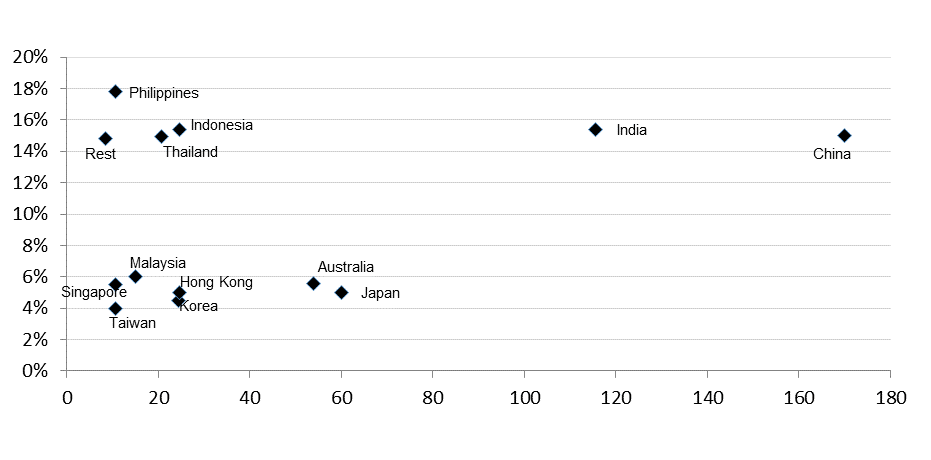

Source: Asian Banker Research Retail financial services in developing markets grew on average by 13% annually to 2015. However there have been dramatic changes since 2014. The fastest growing markets up to 2013 were Thailand and China which experienced annual growth of over 20%. Both markets have been slowing down in line with wider economic woes and we expect retail financial services in these markets in the next few years to grow at a slower pace. Fig. 2: Amongst emerging markets Malaysia expected to see the slowest income growth and Philippines the strongest, while China will continue to generate the highest income by 2020 Expected Growth Rates 2015-2020e (CAGR) and Total Income Generated by 2020e

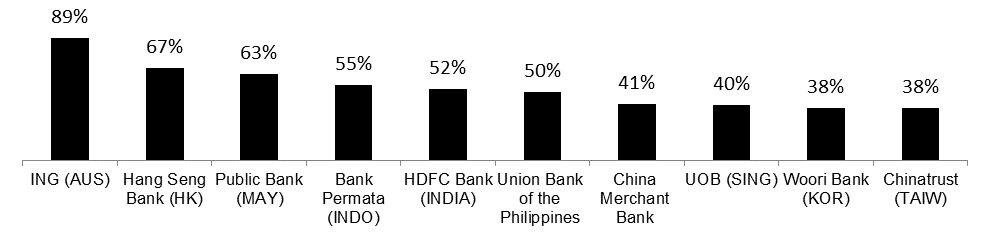

Source: Asian Banker Research Since 2014, the Philippines has outpaced China and Thailand and is becoming one of the key growth engines in the Asia Pacific. Retail banking income is shifting to focus on high yield businesses but tightening of consumer banking regulations to protect consumers is a key threat. The greatest change in regulations is a shift away from a principle based regulatory framework to a rule based framework. As a result regulators have much more power to intervene. In particular, in emerging markets, financial authorities often want to control everything down to the product level, including loan pricing and fee income. Commercial banks have managed the impact of new regulations imposed on banks’ wealth management businesses in the aftermath of the global financial crisis but a second wave of regulatory scrutiny, initiated in 2012, into interest rates and fee structures, compounded by recent macro-economic weaknesses, continues to pose ongoing threats to income expansion. “Regulators are increasingly worried about rising consumer debt so have resorted to tightening unsecured lending, credit cards and home loans. In addition, consumer protection and optionality, which requires banks to seek a customer’s consent to opt in or out of services, are becoming key agenda items for financial regulators in this region,” said Kazmi. In Korea, a toxic mix of an economic slowdown, tightening loan regulation, and rising levels of non-performing loans has sent retail banking income into a tailspin, and the industry will take at least until mid 2016 to reverse the decline. In China and India, regulators are further liberalizing the market. In China, interest rate liberalization coupled with inadequate preparation by banks with poor capabilities in deposit pricing, and the credit risk from the economic downturn, are the two biggest concerns in 2015 for banks that engage in retail financial services. In addition, Chinese regulators have tightened down payments on secondary mortgages and will raise the liquidity coverage ratio (a measurement comparing liquid assets to total net cash outflows over a 30-day period) to 60% by the end of this year and at 100% by the end of 2018. The Australian retail financial services industry is facing increasing pressure on pricing transparency, fee charging structures and the requirement for customer consent for certain services such as contactless payment features. In addition, another round of fines and regulatory measures are looming should incidences of disruption caused by outdated IT systems and banking platforms continue to occur in the future. Over the past decade, commercial banks have increasingly relied on the contribution of consumer banking income which grew from the low teens to 36% on average by 2014. Going forward, shrinking margins and saturated markets will force banks to seek new sources of income in higher yielding business such as personal loans, SME banking, wealth management and insurance. While most banks in emerging markets still have room to grow in the SME segment and have been ramping up their business capacities in this area, SME banking is unlikely to become a major income source in the medium term. Many SMEs are experiencing the damaging effects of weaker economies too, in particular small SMEs with an asset size of less than $1.5 million which often make up more than 70% of all SMEs in a country. This segment of the loan book is currently a concern to many banks. Of equal importance to the retail financial services industry remains the expansion of retail fee income. “Despite improvements in recent years, fee income is still based mainly on transactional based fee income such as ATM usage, fund transfers and payments. Retail financial services markets are still at an early stage in terms of raising fee income from advisory services in wealth segments, that is from segments below private banking, and often see better opportunities for returns by penetrating underserved markets with bancassurance and basic investment products such as mutual funds,” explained Kazmi. Fig. 3: A contribution from retail income in excess of 40% is achieved by top banks Contribution of Retail banking Income to Total Bank Income (%)

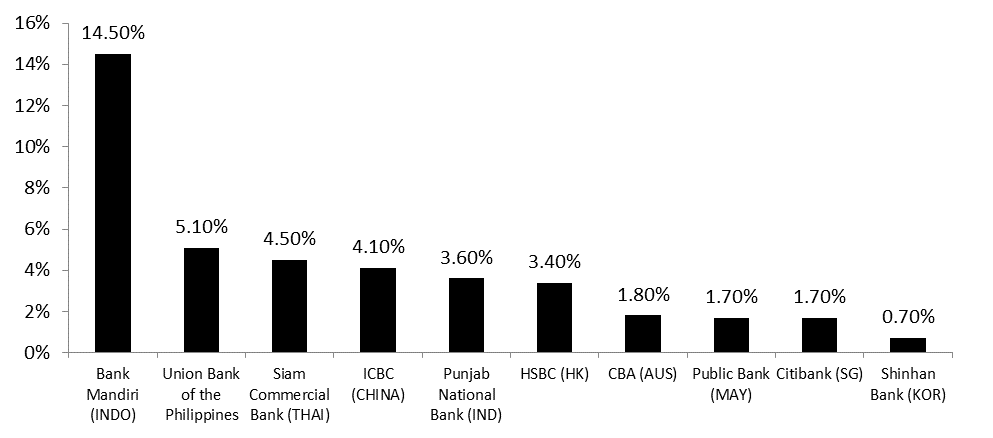

Profitability has declined materially in the post financial crisis era. Retail profitability measured by the return on retail banking assets has decreased from 2.6% to 1.0% on average since 2010 for Japan, Singapore, Australia, Hong Kong, Taiwan and Korea although there has been a slight recovery; at the of end 2014 the figure was 1.2%. The most profitable retail financial services market in this group is Hong Kong with an average ROA of 2.2%. The most profitable retail banks in Asia Pacific are based in emerging markets and led by Bank Mandiri (Indonesia), Union Bank of the Philippines and Siam Commercial Bank (Thailand) (Fig 4.) Fig. 4: The most profitable retail banks in Asia Pacific are to be found in emerging markets Return on Total Retail Banking Assets (Top Bank by Country) In China, the decline of profitability in retail financial services has been the most visible; average retail ROA declined from 2.8% in 2010 to 2% by end of 2014. India’s retail financial services market continues to maintain a high 2.7% ROA, having lost only 10 basis points compared to 2013. Indonesia stands out as the most profitable market with an average retail ROA of 4.9%, driven by its large microfinance and consumer finance market. However, the country has also has one of the widest variances in retail profitability ranging from CIMB Niaga (0.4%) to Bank Mandiri (14.5%). Another impact on profitability has been regulations meted out to the industry that have become omnipresent, costly and time consuming. The increasing levels of investigations of the retail banking sector by regulators in areas such as price setting, transparency and fair treatment of customers will likely maintain the already rising cost of compliance for years to come. All this will force banks to aim to take out further substantial amounts of cost from the system. This will likely intensify business process automation as banks look for operational efficiencies. Categories: Keywords:Yuan, Devaluation, Financial Markets, RenminbiWorld 2015, Cash Mobility, Cross-Border Transaction, PBoC |