The goal of achieving greater payment integration and connectivity among the ten ASEAN member countries by 2025, took a significant step forward when the Working Committee on Payment and Settlement Systems (WC-PSS) completed the implementing policy guidelines (IPG) of the ASEAN payments policy framework for cross-border real-time retail payments and the draft guidelines for updating the annex on use cases of the IPG.

Meanwhile, member countries have taken steps to advance cross-border interoperability of standardised quick response (QR) code for payments and introduce innovative real-time remittances. In particular, the integration of the real time payment systems between countries, suc as the full implementation of the Singapore-Thailand linkage, and partial implementation between Laos-Thailand and Cambodia-Thailand linkages. The Singapore-Thailand real-time retail payment system linkage is expected to go live by the first half of 2021. Payment integration, in so far as adoption of common guidelines and standards such as ISO 20022 and QR codes, will facilitate interoperability between different domestic systems. This is critical to streamline processes, ie. for identity verification and regulatory compliance will ensure greater transparency and security of transactions. It will also enable shorter clearing and settlement cycles for cross-border retail payments as well as wholesale clearing and settlement of financial market and exchange related transactions.

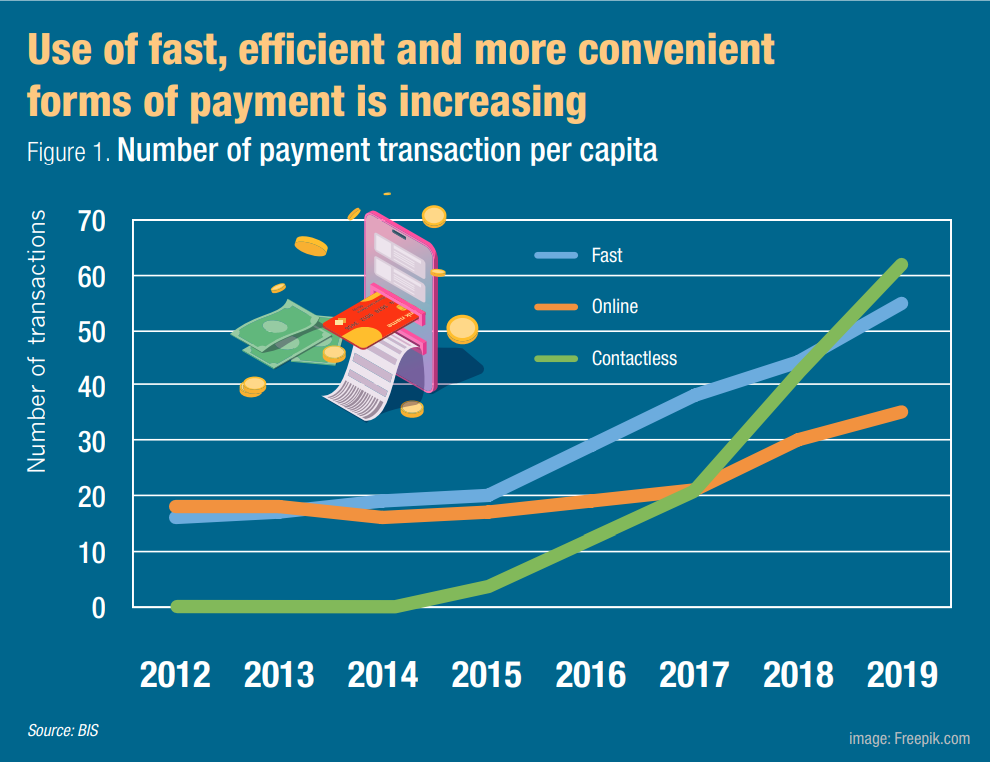

The increasing digitalisation of the financial sectors in ASEAN will catalyse and accelerate the pace of convergence and integration of the disparate systems that exist in the region. This includes the introduction of digital and open application programming interface (API)-based banking frameworks in a growing list of countries as well as exploration into the use of distributed ledger technology (DLT) to create new faster, more efficient and convenient payment infrastructures. In the latest release of the Committee on Payments and Market Infrastructures (CPMI) Red Book statistics, the Bank for International Settlement (BIS) highlighted the rise in adoption and usage of digital payments with consumers increasingly shifting from physical to digital instruments.

Between 2012 and 2019, it observed that more than half of the CPMI countries have experienced a decline in the use of physical payment instruments and an increase in digital payments.

Apart from governments and central banks driving the creation of new payment infrastructures, the private sector is also playing an important leading role in migrating the sector to the new common standards and technologies.

For example, SWIFT has been a prime mover to enable ISO 20022 messages for cross-border payments and cash reporting businesses by the end of 2022, one year later than scheduled as a result of a COVID-19 deferment. However, the deadline for the full implementation of ISO 20022 remains by November 2025, when the current SWIFT MT messages will be replaced by a new API-based exchange.

SWIFT has leveraged its gpi instant initiative to transform payments and securities processing by retooling cross-border infrastructure to enable financial institutions to deliver instant and frictionless end-to-end transactions through connecting domestic real-time payment systems. Beside SWIFT, global payment network processors Visa and Mastercard are also moving into the cross-border real-time and business-to-business payment space to provide alternatives. There are also initiatives by private and public sector players such as Ripple, R3 as well as the Monetary Authority of Singapore and its Ubin project to create new DLT-based payment infrastructures and protocols.

With the deluge of private-public initiatives on offer and in the pipelines, there are many possible routes to achieve the goal of regional payment integration, it is important for authorities to keep their approach and option open and flexible.

All Comments