- A comparison of the profitability of digital banks has been conducted and the payback period assessed

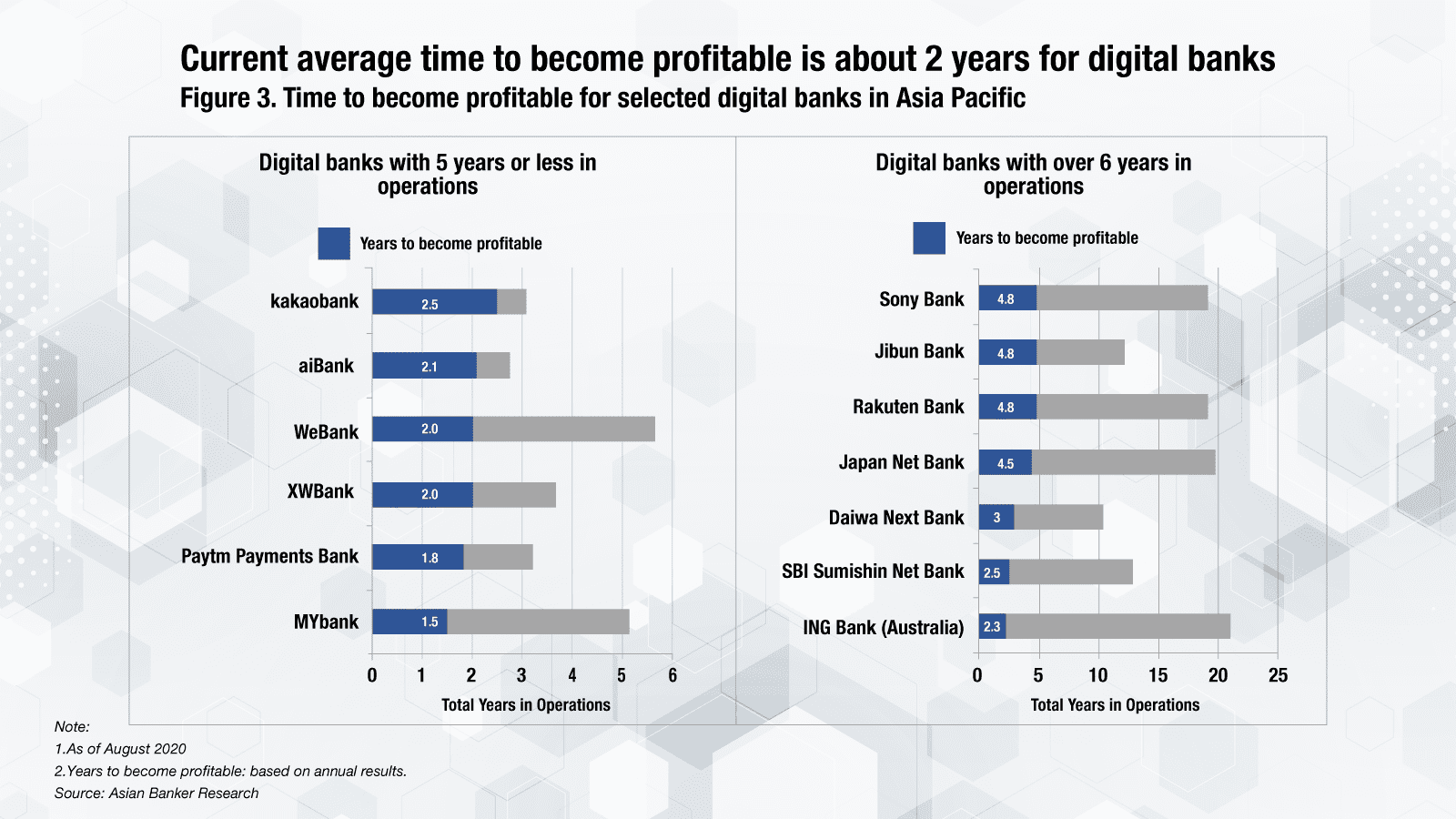

- Current average time to become profitable is about 2 years for digital banks

- Digital banks are better positioned to provide financial services to customers during the pandemic

Customer acquisition is a top priority for digital banks in the early stages of development, and they turn their attention to becoming profitable as they mature. The operating environment for digital banks varies across different markets. While profitability remains a challenge for most digital banks, some digital banks in Australia, China, India, Japan and South Korea have reached profitability.

The aggregate net profit of the thirteen digital banks in Asia Pacific assessed increased by 49% to $1.66 billion in the financial year (FY) 2019 from $1.12 billion in the year before (Figure 1). This is largely driven by WeBank, MYbank, XWBank and aiBank in China. Among these thirteen digital banks, Tencent-backed WeBank posted the highest net profit of $565 million in FY2019, followed by ING Bank (Australia) and Alibaba-backed MYbank. Both WeBank and MYbank reported a full-year net profit for the first time in FY2016.

WeBank saw its net profit increase by 261% in FY2017, 71% in FY2018 and 60% in FY2019. It has leveraged Tencent’s ecosystem, technology capabilities and research and development (R&D) resources, which enabled it to scale up rapidly. In FY2019, investment into technology R&D accounted for almost 10% of its operating revenue, and about 60% of its employees are on the technology side. Leveraging Alipay’s artificial intelligence, computing and risk management technologies, MYbank has cooperated with over 400 financial institutions, serving 29 million small and micro businesses as of June 2020. The number of customers served went up by 70% in FY2019, and 80% of its loan users had previously never received business loans from traditional banks. The bank’s net profit surged by 91% in FY 2019 and its non-performing loan ratio remained stable at 1.3%.

On the contrary, net profit of South Korea’s Kakaobank and China’s aiBank was less than $5 million in FY2019, as both booked net profit for the first time in FY2019. Launched in July 2017, Kakaobank posted a net profit of $11.8 million in 2019 after booking a net loss of $97.5 million in 2017 and $18.7 million in 2018. It continued to outperform the country’s first internet-only bank K Bank in terms of profitability. K bank saw its net loss widen from $18.9 million in 2018 to $86 million in 2019. In addition to being more innovative, Kakaobank has also been more successful in tapping fresh sources of capital for their expansion. Kakaobank had a total paid-in capital of $1.6 billion at the end of 2019, compared with K Bank’s $447 million. K Bank began suspending its loan services in April 2019 due to the shortage of capital. Telecommunications giant KT’s application to raise its stake in K Bank was disapproved last year, as it has a history of violating fair trade regulations. In July 2020, BC Card, a subsidiary of KT, was approved to become K Bank's largest shareholder. With its total capital increasing to $760 million, the bank has resumed its lending services in July 2020.

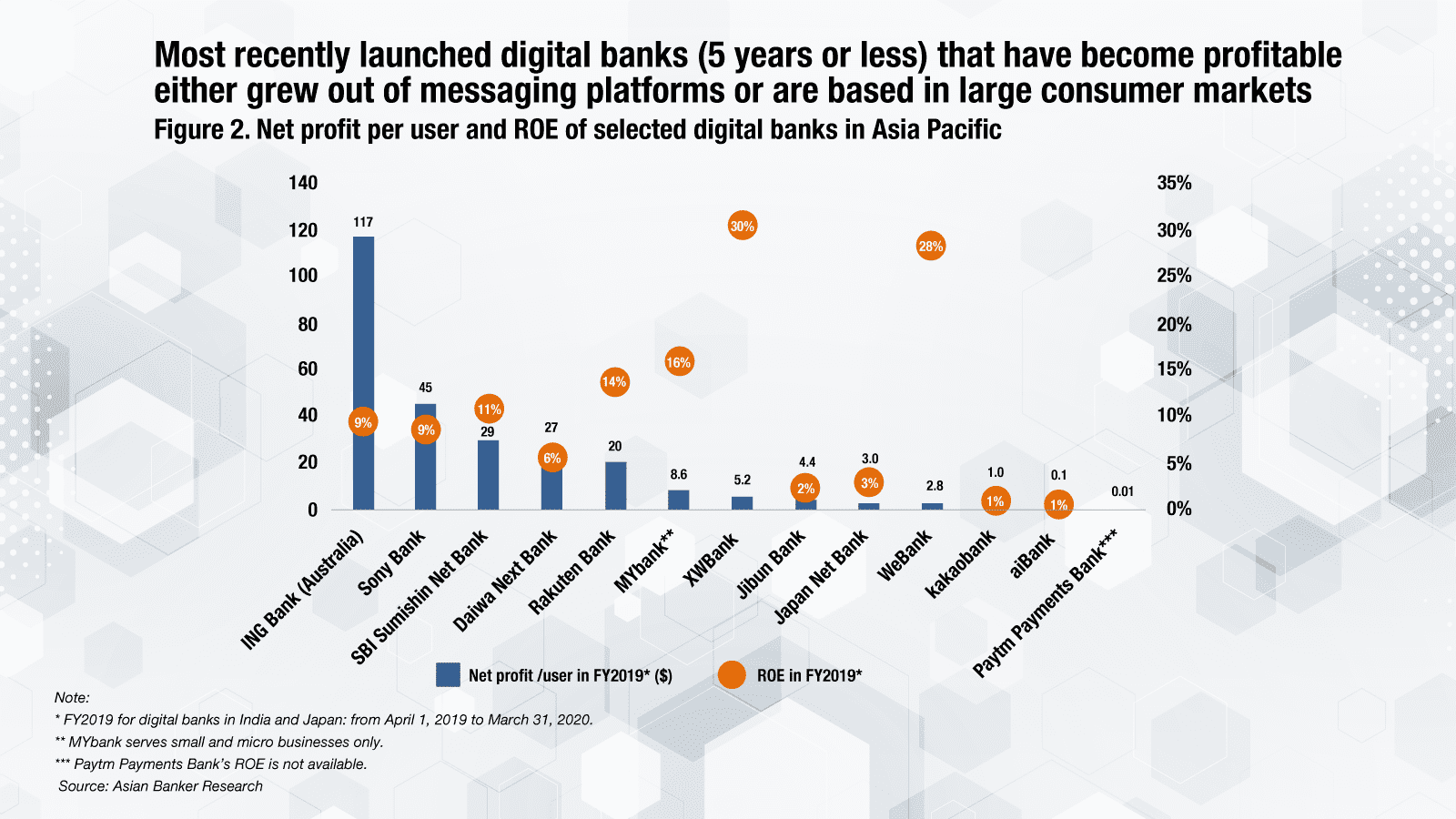

Xiaomi-backed XWBank and MYbank achieved a return on equity (ROE) of 30.3% and 28.2% respectively in FY2019, far outperforming other digital banks (Figure 2). When it comes to net profit per user, there is a huge gap between digital banks in China and the top performer ING Bank (Australia) (Figure 2). At the end of FY2019, ING Bank (Australia) had 2.6 million customers, while XWBank had 31 million customers and WeBank served over 200 million individual customers and 0.9 million small and micro businesses. The digital banks that were launched in the past six years and have turned profitable either grew out of messaging platforms or are based in large consumer markets. WeBank took advantage of Mobile QQ and WeChat, the messaging apps operated by Tencent. Backed by South Korea’s leading messaging platform KakaoTalk, Kakaobank’s customer base has surpassed 12 million in March 2020, which is more than a fifth of the country’s entire population.

India’s Paytm Payments Bank only earned $0.013 net profit per user in FY2019. However, it is the first payments bank in India to turn a profit. It has proved that the segment can be profitable despite the limited revenue streams. Payments banks are not allowed to undertake lending services and can only accept demand deposits up to $1,400 (INR 100,000) per customer. Besides fees earned from transactions, they also invested in government securities. In aggregate, the seven payments banks in India recorded net losses of $90.6 million in the financial year ended March 2019, according to Reserve Bank of India’s Report on Trend and Progress of Banking in India.

Paytm Payments Bank started operations in May 2017, and it is the largest Payments Bank in India in terms of deposits. The bank earned a net profit of $2.7 million in the financial year ended March 2019 after booking a net loss of $3.2 million in the year before. It had a market share of 19% and 32% respectively at the end of March 2019, in terms of mobile banking and Unified Payments Interface (UPI) transactions. The total number of UPI handles on Paytm Payments Bank platform reached 100 million in February 2020, driven by Paytm’s All-in-One QR which accepts payments from all UPI-based platforms. In the financial year ended March 2020, its net profit went up by 55% thanks to higher customer acquisition in smaller cities and towns.

When comparing how long it took these digital banks to break even, it was determined that digital banks with 5 years or less in operations have managed to turn a profit in a shorter period (Figure 3). This can be partially attributed to the new technologies and growing demands. On average, it took them around two years to turn profitable, compared with over four years for the first generation of internet banks that were introduced in Japan such as Japan Net Bank, Rakuten Bank and Sony Bank.

By comparison, digital banks in Australia are not expected to become profitable within two years. In 2019, Australia’s new entrants like Judo Bank, Volt, Xinja and 86 400 secured the full authorised deposit-taking institution (ADI) licence and IN1Bank received a restricted ADI licence. Judo Bank became the first Australian challenger bank to reach the AU$1 billion ($650 million) valuation and attain unicorn status after it raised $148 million in Series C funding round in May 2020. Although these digital banks are attracting more and more customers, profitability remains a challenge.

Digital banks are better positioned to provide financial services to customers during this COVID-19 period thanks to their digital business model. In Japan and South Korea, digital banks have performed better than traditional banks in terms of net profit. In the first half of 2020, combined net profit of South Korean banks fell by 17.5% as their allowance for loan loss reserves increased by 157%. However, Kakaobank witnessed a 372% surge in its net profit in the first half of 2020, driven by robust lending business and partnership with securities firms and credit card companies. In Japan, those six digital banks’ aggregate net profit went up by 8% in the quarter ended June 30, 2020, while three largest banking group saw their combined net profit plunge 49%.

Chinese digital banks are expected to deliver weaker performance for 2020, as financial institutions have been pushed to sacrifice $212 billion (RMB 1.5 trillion) in profit this year to support companies by lowering lending rates, cutting fees, deferring loan payments and granting more unsecured loans to small businesses. In the first half of 2020, combined net profit of Chinese banks declined by 9.4%. XWbank recorded 14.5% decline in its net profit in the first half of 2020. In addition to the requirements on limiting the profit, the bank also slowed down the expansion. At the end of June 2020, its assets and liabilities dropped by 9.2% and 11.2% respectively from the end of December 2019. It is expected that the profitability of digital banks in China will be better in 2021 as the economy gradually recovers.

The competition grows as traditional banks continue their digital transformation and more digital banks will enter the markets. Most digital banks continue expanding their customer base and introducing innovative products and services, especially those most recently launched digital banks. Overall, their growth outlook remains optimistic.

All Comments