- API is a set of commands that allows software applications to talk with each other in a seamless manner

- There has been a surge in the number of APIs across industries in the past five years

- Open APIs will enable more companies to link their products or services to banks while still keeping confidential data secure

For many consumers, Application Programming Interfaces (APIs) enable access to services without them even realising that they are at work in the background. Restaurants use APIs to link their websites to Google Maps, while Travelocity and other travel sites use APIs to enable consumers to choose their best travel options. Companies ranging from Uber and Airbnb to the BBC and FedEx also use APIs to improve customer experience.

However, in the financial services industry, that type of cross-business collaboration has been scarce. As competition increases and fintechs compete with banks for customers, leading institutions are starting to open up their APIs to gain a competitive advantage.

How do APIs work?

According to the Monetary Authority of Singapore (MAS), which is actively pushing the use of APIs, an API is a set of commands that allows software applications to talk with each other in a seamless manner. Visa similarly describes an API as a set of routines, protocols and tools for building software applications, which is typically used to expose data or services that can be used by other applications.

Citibank’s managing head of global product development Sanjeev Mehra explained that APIs allow software of various organisations to talk to each other without the firms acquiring deep domain knowledge of each other. Whereas companies used to have programmers with detailed banking knowledge to create simple applications, with APIs software developers can now easily create programmes which are intelligent and self-sufficient.

For example, when a consumer opens an app to request a ride from a car hailing service and clicks “Yes”, the location pin on the map is the result of a call to a third-party map API. When the consumer arrives at the destination and pays for the ride with the app, he is experiencing another call to a payment service API.

APIs can be used in almost any industry and, as Accenture noted in Driving Innovation in Payments: “APIs have a nearly-20-year history helping progressive companies like Salesforce, eBay and Amazon transform industries, open up new opportunities and improve rewards against risks of the digital world.” PayPal was one of the first adopters of open APIs for financial services more than a decade ago, when it opened up its APIs to third-party developers in 2004.

However, banks have until recently been reluctant to set up open APIs. As a result, disruptive innovators such as fintechs have been and still are more likely to establish open APIs to stimulate new businesses.

According to Accenture, the new innovators are using APIs as an approach to business development that supports new dialogue between customers, suppliers and partners in emerging business ecosystems. It stimulates innovation through interconnected API-driven communities that have been adopted by the media, travel, hospitality and retailing industries.

The benefits of APIs

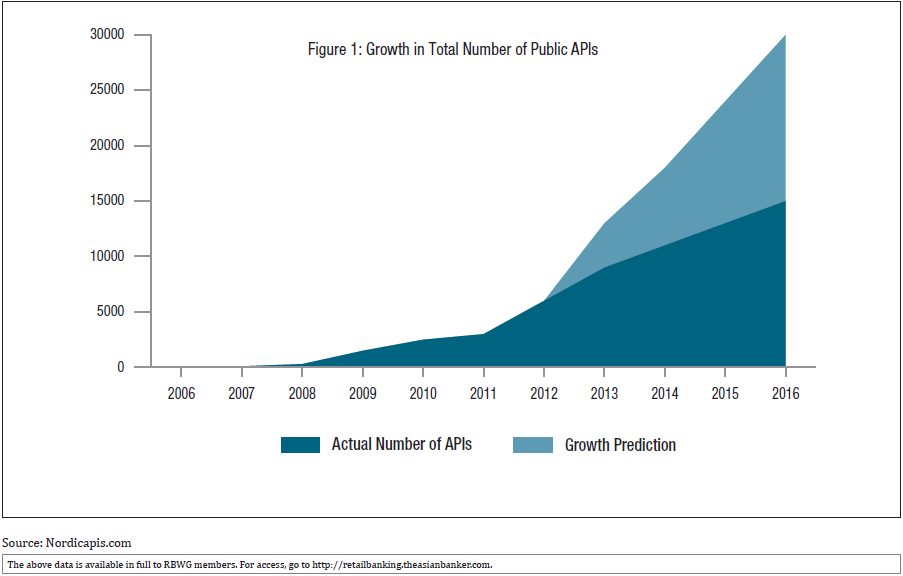

While growth in the number of public APIs has not been as rapid as was forecast, there has been a surge in APIs over the past five years as more companies have discovered the value of APIs (Figure 1).

The number of APIs across industries has skyrocketed over the past five years

The impact of APIs can be huge. Babson College professor Bala Iyer and Boston College associate professor Mohan Subramaniam found that there are more than 12,000 APIs offered by firms today, and other estimates are even higher. Salesforce.com reportedly generates 50% of its revenue through APIs, Expedia.com generates 90%, and eBay 60%.

The core advantage of an ecosystem built around APIs according to MAS’ chief fintech officer Sopnendu Mohanty, is the ease of collaboration and co-creation between industry players, which engenders new ideas and innovative solutions. “By adopting open APIs, traditional financial institutions can more readily experiment, collaborate and leverage on innovative solutions and business models that other participants in the financial ecosystem have developed,” he said.

For consumers, open APIs enable the sharing of information securely without having to reveal their passwords. It is the same technology that allows consumers to sign into other online accounts using a separate account such as Facebook or that tells an Uber driver who and where they are.

More broadly, technology provider Cognizant said in its Banking as a Service white paper that APIs allow banks to share data with internal evelopers, partners and third-parties such as fintechs, which then manipulate this data to offer services such as mobile payment apps or peer-to-peer lending solutions. Banks can also use open APIs to tap into external innovation, enhance the customer experience, improve customer loyalty or increase their wallet share.

While APIs can be used in many parts of retail banking, Cognizant found that the greatest impact is in four areas: funds transfer and digital payments, to enable money transfers; cross-border transactions, where APIs enhance security; perks and reward packages, where merchants and banks partner on offerings; and APIs portfolio dashboards, which provides a snapshot of the customer’s financial situation.

Banks grow their businesses with open APIs BBVA’s API Market, for instance, enables businesses to link to the bank more easily. Some APIs can enable businesses to create a new chequing account or access account data, while others allow businesses to register their customers at BBVA bank so that they can offer them accounts and other white label banking products. Businesses can also use APIs to receive or send money using BBVA’s transfer capabilities, or to make payments within their platform.

In the US, PNC Bank opened up its APIs to provide the comprehensive programming tools required to integrate payments into a custom website or other ecommerce applications. This API accommodates many standard programming languages, allowing integration with ease and transaction security.

In Europe, Fidor Bank has open APIs which it said enable efficient and secure access to systems and services in order to connect business processes and create value chains across organisations. Open APIs support a lot of functions around banking and payment, as well as many community features and third party services.

Along with APIs from individual banks, there are industry-wide initiatives for open APIs. The Open Bank Project, for instance, is an open source API and App store for banks that enables financial institutions to securely and rapidly enhance their digital offerings using an ecosystem of third party applications and services. A key advantage is that it exposes transaction data in a simple and consistent structure by abstracting away the peculiarities of each banking system and using “connectors” that interface between the OBP API and each banking system.

While some financial institutions may be reluctant to go as far as these leaders and open up their APIs, Bain & Company concluded that banks that do not open up their APIs could leave themselves vulnerable to disintermediation. One scenario it offers is that massive change occurs in customer-facing activities across most profit pools, leading to “game over” for banks’ distribution channels. Leading technology firms with high credibility among consumers, such as Apple and Google, could then take over the main customer relationship.

Regulatory requirements for open APIs

While banks may face competitive pressure if they do not open up their APIs, they may also be forced by regulators to offer open APIs before long.

In the UK, for instance, the Competition and Markets Authority’s (CMA) retail banking market investigation concluded that older and larger banks do not have to compete hard enough for customers’ business, and smaller and newer banks find it difficult to grow. “This means that many people are paying more than they should and are not benefiting from new services,” the CMA concluded. “To tackle these problems, the CMA is implementing a wide-reaching package of reforms.

Central to the CMA’s remedies are measures to ensure that customers benefit from technological advances and that new entrants and smaller providers are able to compete more fairly.”

A similar change is underway across Europe. Although the revised Directive on Payment Services (PSD2) does not explicitly refer to APIs, BBVA platform evangelist José Manuel de la Chica commented that “most experts in the technology and financial sector take it for granted that APIs will be the technical means that allow the banks to fulfil the specifications of the regulation, quite apart from what the EU countries implement in their respective legislations during the coming months.” PSD2 may be the next step that propels banks towards open APIs.

Taking a somewhat softer approach, MAS in Singapore published a “Finance-as-a-Service API Playbook”, which MAS managing director Ravi Menon said: “Provides guidance on common and useful APIs that FIs could make available.” The Playbook also provides guidance for the standardisation of APIs, data exchange and governance mechanisms.

Case studies for APIs

Citi

In November 2016, Citibank launched a new global API developer portal to connect with developers and enable them to build innovative client solutions faster. These open APIs are a means to an end and is part of a much bigger picture: “If we bankers are to thrive in this new world, there has to be a broader strategy,” said Citibank’s Mehra. He referred to three levels of such a strategy; one is organisational change, another is a technology reboot, and the third is opening up. Open APIs are essential for that third piece, opening up, and key opportunities would come from fintechs and incumbent banks working together for “fintegration.”

Indeed, the API strategy for the bank falls right into fintegration. The industry created a lot of standards around APIs, so any firm can use it. For example, a retailer such as Amazon can take a credit card points API and embed it into its sites without the knowledge of Citi, and gives customers the option to pay with points.

Another key driver for open APIs is the way banks sell and distribute. Whereas banks currently use traditional channels such as branches and call centres, APIs allow them to open up services through third party apps or platforms and give options to customers.

“The advantage will be with early movers, who should be able to grab mindshare of programmers. We’re entering the era of the API economy. Not having an API would be like not having www (world wide web) in the early 2000s. Incumbent banks who have multimarket presence will have an advantage,” explained Mehra.

In prioritising which APIs to open up, the bank used two parameters: customer usage and value. Citibank started by looking at customer usage data and found that about 60 out of the 1,200 to1,500 processes in consumer banking accounted for more than 80% of customer interactions. Second, other transactions such as acquisition or advisory services have high value, even if they are not high volume. Using those insights, “we created a backlog of APIs to build. They include account services such as transaction inquiry, card inquiry, offers, payments, transfers and rewards.”

While the bank is still in the early stages of implementing the strategy, it has received more than 1800 registrations from small software companies to large organisations. Each one is being reviewed to make sure it makes commercial and brand sense. One perhaps-surprising example is Honestbee, making Citibank a partner with an online grocery and delivery company.

The bank is also making sure it is part of the customer’s preferred ecosystem in each market, such as WeChat in China and Line in Thailand.

The other big area that APIs have opened up is the ability for large partners to be able to do white label partnerships. While such partnerships historically such had a long gestation period, Mehra said organisations can do white label with APIs in a short period. “This is a kind of landscape shift.”

OCBC

“Open APIs present opportunities for banks to help create a better service delivery and experience for customers and end users,” said OCBC Bank’s senior vice president Praveen Raina. “It is also about being social. We want to create a ‘data social network’ which facilitates a free flow of certain non-customer data that will benefit any third-party and the community as a whole,” he added.

The bank’s open API platform was developed in-house and will bring significant cost savings for OCBC as well as for third-party software developers. “We minimise the effort required to tap on our information, allowing developers to focus on the issues that matter – creating innovative solutions,” he remarked.

Since the initial launch with four open APIs in May 2016, OCBC has progressively rolled out more and has now released 22 open APIs. The bank had 270 sign-ups within just two days of launch, and by January 2017 it had received more than 700 sign-ups and approximately 30,000 API requests. Some firms are using APIs for services such credit cards, for example, and a local travel company uses the foreign exchange rates API to display travel deals with real-time currency rates.

APIs provide faster time to market because they can be easily integrated into both new and existing applications. Raina said that gaining access to information about OCBC’s products and services enables software developers to embed the details into their applications.

APIs also allow information to be updated more accurately and in real-time, eliminating the need for software developers to check manually for updates. The platform contains features that are currently considered best ractice for developer engagement including self-serve registration, instant API access, a “sandbox” testing environment, documentation, code snippets and reference applications.

APIs present a competitive advantage

While banks have had a longstanding tradition of protecting information or services, the new economy requires an entirely different approach. Banks that offer open APIs will enable more companies to link their products or services to the bank while still keeping confidential data secure.

Banks that do not offer open APIs, on the other hand, are far less likely to create those strong links. The advantage will be with early movers and grabbing the mindshare of other companies as well as programmers now so that they can link consumers to the bank will enable competitive advantage that lasts far into the future.

All Comments