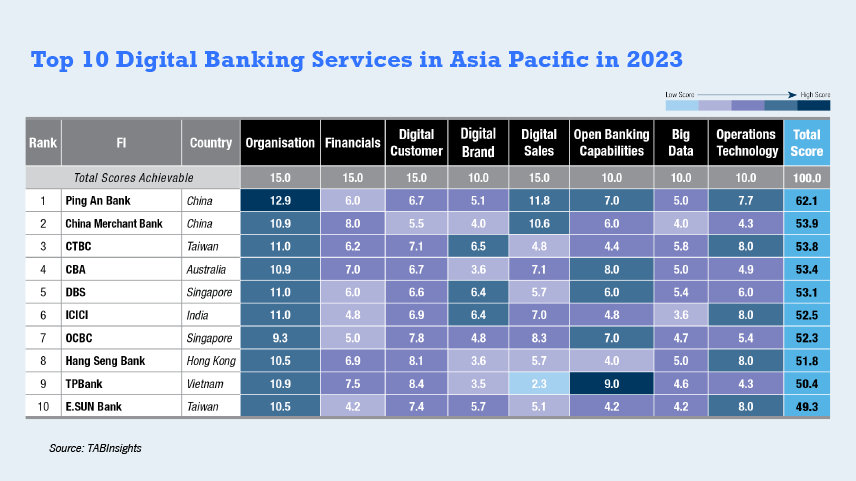

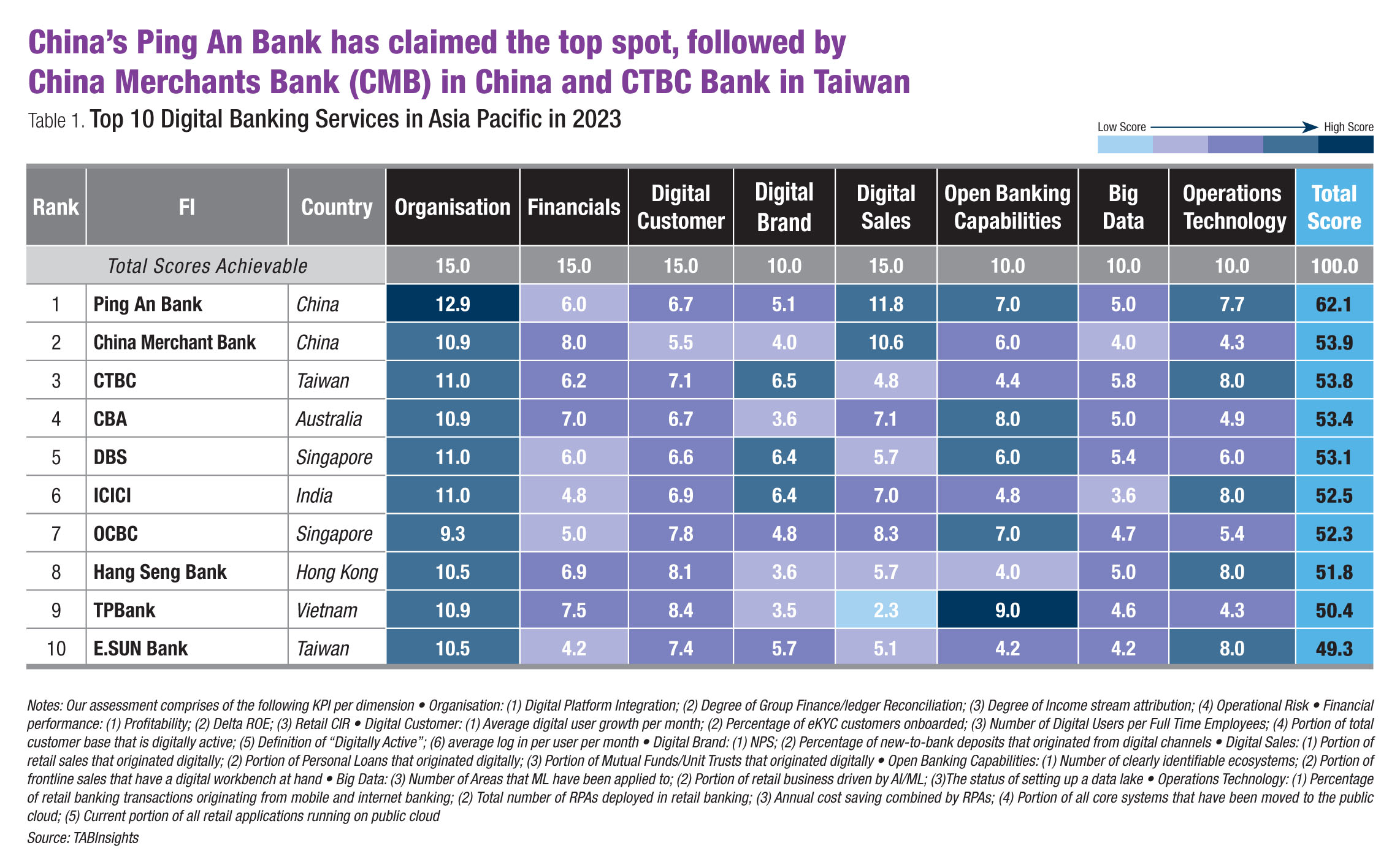

This year’s Top 10 Digital Banking Services ranking focuses on the digitalisation efforts of commercial banks, and the results are instructive to the industry.

Banks have demonstrated considerable improvements not only by digitalising their products, services and customer onboarding, but transforming their entire franchise as well. This transformation has been achieved through a focus on organisational agility and simplification, automation and improving the overall consumer experience.

The assessment takes into account eight key dimensions covering organisation, financial performance, the digital customer, digital brand and sales, open banking capabilities, big data capabilities as well as operations and technology.

Ping An Bank excelled in various areas, including progress it made in digital transformation, expanding its open banking platform, improving digital sales, launching Al and cloud enabled customer-centric digital initiatives and seamlessly integrating its digital and physical touchpoints.

It achieved this by leveraging a robust application programming interface (API) gateway with over 240 existing APIs, further strengthening its open banking platform. Furthermore, the bank demonstrated its leadership in digital sales by achieving 72% of digitally-originated sales across seven major top-line product categories—among the highest in the region. Its digital banking architecture is supported by 95% migration to private cloud and the support of more than 100 RPAs.

Significant portion of investment has gone into omni-channel integration and open banking capabilities

The integration of digital and physical channels has become a key priority for banks as customers expect to be able to access their accounts and conduct transactions through multiple channels. By connecting multiple touchpoints such as physical automated teller machines (ATMs) and branches to mobile apps and 24/7 online services, banks have integrated physical and digital access points to reduce friction and to create a more user-friendly, intuitive, and unified user experience.

Customer journeys are never fully digital nor fully physical and in most cases involve some degree of both. Providing those frictionless handshakes from one channel to another is critical.

While a grand omnichannel integration is still years ahead, banks have been focusing on specific journeys such as withdrawal of cash on the entire ATM network with a QR code, e-ticketing to reserve a branch ticket via the mobile app to track branch traffic and minimise waiting time, seamless handshake from a chatbot to a call centre agent, or beginning a home financing journey on mobile and signing the loan offer at a branch.

Banks are also designing products and services with partners who can deliver more progressive and strategic support via open banking and APIs. By complementing their core offerings with specific add-on capabilities, banks can offer more competitive value propositions to customers.

While this has been fairly established in payments, we see banks taking first steps to address the needs of customers in a more comprehensive way.

For instance, backed by strong API gateways, banks have established open-ended wealth platforms to connect partners from the capital and asset management industry to provide curated content more flexibly in the form of images and texts, videos, and livestreaming services, but also quickly view and analyse modularised data on the wealth portal.

In building home financing ecosystems, CBA in Australia developed seven key services of which two are proprietary and five are integrated third-party solutions. They range from a home-buying assistant (conveyancing) that is integrated in the mobile app, to government-funded green loans, as well as access to wholesale energy prices and telecommunication services.

TPBank in Vietnam offers over 20 services on their eBank platform, connecting to more than 50 partners via open API across financial and non-financial industries. These service providers include financial firms like securities and insurance companies, and those in the lifestyle and health sectors. With this in place, the bank has onboarded close to a third of its newly acquired customers in 2022 from its digital ecosystems.

Smart campaign automation engines deployed to personalise marketing and communications journey

Financial institutions can no longer rely on a one-size-fits-all approach. Banks must have a much stronger understanding of their customers, the ability to analyse and predict their needs, and provide proactive services tailored to their preferred channels and communication methods.

Deeper insights into customer transactions, profiles, behaviour patterns, and predictive analytics can enable more precise marketing, intelligent campaigns, and customer service.

Several banks across the region are expanding use. With iterative development and refinement, smart automation engines based on AI models have the potential to boost conversion rates by threefold on average across business lines.

Core banking architecture prioritised in digital transformation

Legacy infrastructure and monolithic architecture have consequently led to struggles in meeting the exponential rise in volumes of digital and real-time transactions. To counter this, banks are now focusing on synergising their current private cloud with the public cloud to better scale and reuse their systems.

Back-end technology and legacy modernisations have become key priorities for banks. More and more favour a leaner core by moving systems out of the existing core and using modular microservice systems that increase agility and workflow.

Banks are also taking other processes, mostly non-essential workloads, out of the core system, including ‘Off-Us’ transactions, lending origination, rule engine for credit processes, and retail lending.

Institutions are also migrating a significant portion of processes to the cloud in the short- to medium-term, though some players prefer a private cloud strategy to address data control and security concerns.

Despite the nimbleness of off-premise strategies, a portion of banks remains cautious about how much of the expanded workload can essentially move to the cloud. Cloud providers charge by data volume and banks could end up paying more compared to what they can support conventionally on premise.

Click here to see the full Digital Banking Services in Asia Pacific 2023

All Comments