- The target market for robo-advisors ranges from the average investor to high net worth individuals

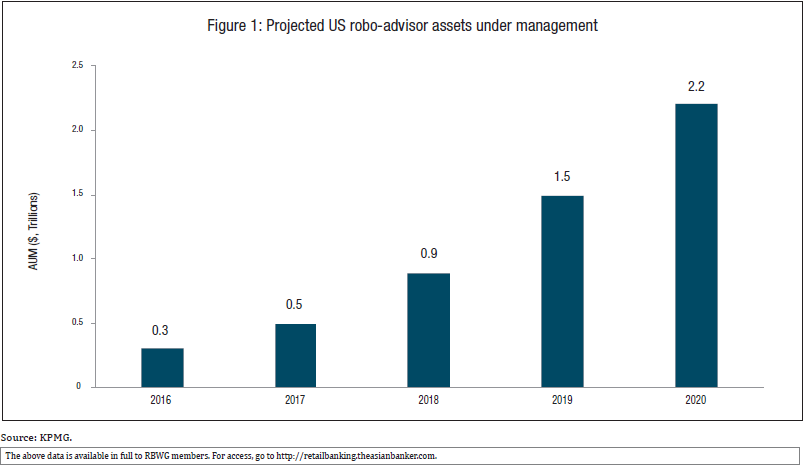

- Assets under management managed by roboadvisors is expected to grow to $2.2 trillion by 2020

- Digitisation initiatives by both banks and fintechs are expanding rapidly in Asia to provide customers with better robo-advisors

The term “robo-advisors” refers to digital investment advisory services that rovide customised investment advice or portfolios using algorithms and other software tools. Customers usually fill in an online questionnaire that asks about their investment preferences and risk profile. The robo-adviser then uses algorithms to offer investment advice as well as to rebalance the portfolio regularly.

The target market for robo-advisors ranges from the average investor, who more often uses an independent robo-advisor, to high net worth individuals (HNWIs), whose private banker may use a robo-advisor in a hybrid model.

A key advantage of robo-advisors is that customers receive independent investment advice and more choices at a fraction of the cost of traditional financial advisors. Fees are usually less than one percent, compared to the 2% to 3% that traditional advisors in Asia often charge. Along with giving customers high-quality advice round the clock and at low cost, robo-advisors can reduce the behavioural biases of traditional portfolio managers and provide customised investment tools.

The attraction of robo-advisors

Perhaps surprisingly, robo-advisors were first developed during the financial crisis around 2008. “Friends and family asked me, ‘What should I do with my money’,” said US-based Betterment founder Jon Stein, one of the early pioneers in the industry. “There were no good answers – so I set out to build one.”

Betterment and other firms started building robo- advisors that could help customers select investments and rebalance their portfolio periodically. Mint’s sale to Intuit in 2009 for about $170 million showed just how attractive these new robo-advisors had become, leading even more start-ups to jump in to develop more options.

Assets under management (AUM) managed by robo- advisors is expected to grow rapidly over the next half-decade, driven by consumers who are becoming more comfortable with robo-advisors and the higher quality of their services they are providing (Figure 1).

By 2020, AUM managed by digital advice platforms will reach $2.2 trillion

Today, there are dozens of robo-advisor developers and firms around the globe.

Seeing their wealthy clients flirt with robo-advisers, financial institutions are racing to release their own automated investing technology. Kendra Thompson, managing director of Accenture, told Bloomberg that the main worry comes from banks “seeing experimentation from people with much larger portfolios, where they are taking a portion of their money and putting them in these offerings to try them out.”

Traditional advisory firms like Charles Schwab, Vanguard, Bank of America, and Credit Suisse have jumped into the game by developing their own robo- advisors internally. Other firms, such as Blackrock and Goldman Sachs, have recently spent hundreds of millions of dollars to acquire robo-advisors too.

Will investors use robo-advisors?

Talk to private bankers and you are likely to come away with the impression that investors will not use robo-advisors. Capgemini found in its Wealth Management Global HNW Insights Survey this year that only 30% of wealth managers believe their HNWI clients would consider having their wealth managed by robo-advisors.

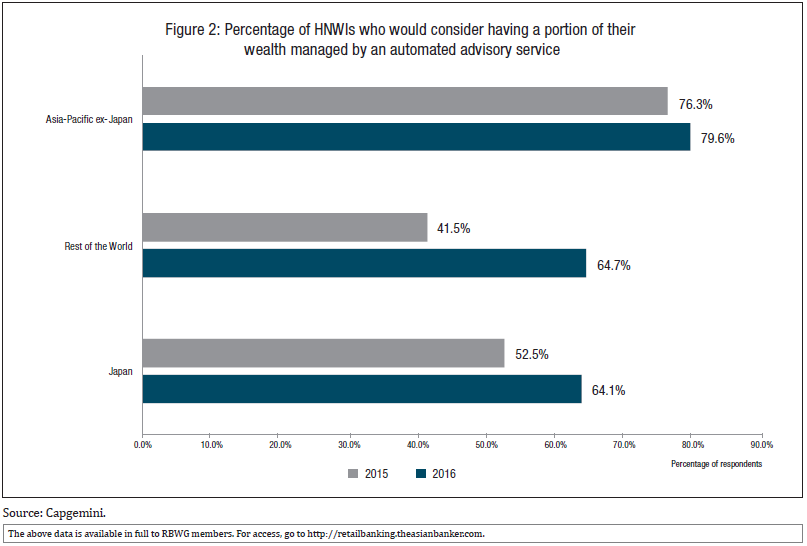

The story is quite different when it comes to investors. Capgemini found that HNWIs demand for automated advisors shot up from 48% last year to 66% this year saying they would use a robo-advisor. The demand is even higher in Asia Pacific at 79%. Moreover, 82% of under-40 high HNWIs and nearly half of over-40 HNWIs expect most or all of their wealth management relationships to be conducted digitally within five years (Figure 2).

While relationship managers at banks believe HNWIs prefer the human touch, the vast majority of HNWIs – say they are comfortable with having their money managed by robo-advisors

While any customer can use a robo adviser, Ernest & Young (EY) found that the sweet spot for robo-advice is the HNWI segment rather than the mass affluent or emerging HNWI segments. Around 71% of HNWIs are likely to consider using a robo-advisor as compared to just 37% of the mass affluent.

These changes are already having a major impact on banks. Royal Bank of Scotland (RBS), for example, announced in March this year that it is eliminating 550 jobs in the UK and replacing staff with robo-advisers.

Robo-advisors in Asia

Given the high level of interest in digital advice, it is no surprise that digitisation initiatives are expanding rapidly in Asia.

Last year, for instance, Credit Suisse launched a global digital private banking platform for clients in Asia that uses a multi-channel service delivery model to increase efficiency and serve clients better. In Japan, Mizuho Bank launched a service that delivers personalised investment advice to investors on their smartphone and personal computers.

This year, DBS Bank leveraged IBM Watson’s cognitive computing technology to roll out Wealth Adviser, which it claims can read research and analyst reports and match them with the clients’ risk appetite, investment objectives, and preferences. OCBC went even further when it launched its OneWealth app, offering everyone from beginners to seasoned investors the ability to obtain customised market information and investment suggestions, monitor their investments and receive personalised mobile alerts. Blackrock is also reportedly looking to enter the Asian robo-advisor market.

Not to be outdone, fintech start-ups are jumping into the fray. Ignition Wealth in Australia, Lingji in China, Chloe in Hong Kong, Theo in Japan, and Smartly and Bambu in Singapore are just several of many firms in Asia that have recently launched or are in the process of launching independent robo-advisors.

Partnerships between longer-established US-based robo-advisors and Asian companies are on the rise as well, with US-based DriveWealth’s partnership with China’s CreditEase being just one example. Even Tencent is looking at offering a wealth management service through its popular WeChat service.

Admittedly, cross-border expansion can be a challenge. As TrueWealth founder Kim Iskyan observed, regulations “can vastly differ from one Asian country to the next. This has limited Asia’s development of automated investment services compared to the West.”

Although robo-advisors are still at a nascent stage, the potential in Asia is huge. In China, for example, China Merchants Securities estimates that assets under management of robo-advisors will grow to $905 billion by 2020. In Hong Kong, Aite Group expects that assets held by robo-advisors will increase from $400 million this year to more than $20 billion by 2020.

Hybrid models

While fintechs offer stand-alone robo-advisory services, banks more often use a hybrid model to provide automated services backed by a relationship manager. A Citi report, Digital Disruption, published this year, stated that “We see the advent of robo- advice as an example of automation improving the productivity of traditional investment advisers, and not a situation where there is significant risk of job substitution.”

Vanguard Group, for example, said its personal advisor services in the US was a response to specific clients’ demand, not to a vague robo-advisor threat. It offers an ongoing client-advisor relationship, with advice ranging from financial behaviour coaching to cash flow analysis, at a 0.30% annual fee.

Robert Shafir, head of private banking and wealth management at Credit Suisse, similarly said that: “Digitalising our private banking services empowers our clients, giving them better access to the knowledge and expertise from across the bank, (and) it also enables greater collaboration with clients, giving relationship managers deeper insight into their clients’ preferences and investment objectives.”

Leading-edge robo-advisor innovation

With nearly a decade of experience under their belts, leading robo-advisors are powering ahead to offer even better services.

The first generation of robo-advisers was designed to eliminate the limitations of traditional wealth managers, such as human interference, and to offer automated investments at a fraction of the cost of traditional advisory services.

The next generation is now starting to introduce more sophisticated services that link financial planning more closely to investment advice and offer customised services that are comparable to most elite managed accounts. The new technology uses intelligent risk management tools to allocate each investor’s portfolio dynamically, based on quantitative measurement of their risk appetite. It can also rebalance asset classes to keep risk constant, so that investors can capitalise on market risk on the upside and limit exposure to excess risk on the downside. While robo-advisors may not offer the full suite of services such as estate planning and tax advice yet, adding these complementary services digitally may well just be a matter of time.

Yseop, for instance, offers multilingual natural language generation software that gives financial institutions the ability to build their own applications so that relationship managers can deliver smart recommendations to their clients.

Likewise, Elm Partners uses value momentum models that combine fundamental analysis with momentum and technical signals, while Quandl handles unstructured non-financial data as well as sentiment and alpha-generating data to make its recommendations.

Another example is Motif Investing, which offers portfolios that reflect a theme or strategy such as high- yield dividends, self-driving cars, or clean technology, in either professional and community-built portfolios, or ones that investors create themselves.

Case Studies

Smartly

Smartly, a robo-advisor headquartered in Singapore, uses smart algorithms to recommend a globally diversified portfolio of exchange-traded funds (ETFs) built on what it says is Nobel-prize winning research. Keir Veskiväli, the company’s chief executive officer, told The Asian Banker that the firm is well on its way to launching its B2C robo-advisor service in Singapore as “the regulatory part is solved”.

To help customers construct a portfolio, Smartly uses score-based investing. “We take you through a risk questionnaire, set up goals, ask questions at the end, the algorithms go to work and we make a

recommendation,” Veskiväli explained. Smartly also utilises games, short animated videos, and quizzes to teach customers about fees, passive investing, and ETFs.

Smartly offers portfolios using global diversified ETFs in Singapore because they are cheap, fluid, offer exposure, and have low fees. Statistically, almost all actively managed funds under-perform. In Indonesia, Vietnam, Malaysia and India, on the other hand, regulatory constraints make it difficult to promote ETFs and Smartly will likely offer other options.

“The whole idea is to make it simple for the end user and understandable for the bottom of the pyramid that nobody is focusing on,” Veskiväli said. “Users can start with us for as low as $50,” he added.

When he meets with banks, Veskiväli noted, the first questions are, “Can I push my product, push fees higher, not educate the customer.” Banks typically charge 2% to 3%, so it is hard for them to start charging less than 1%. Banks should not be scared, he said, because in Asia “the robo model has not proven itself. Players are coming up and most likely they will get bought out.”

Crossbridge Connect

Crossbridge, headquartered in the UK, developed the CONNECT platform to help clients select their investment goals, set a time horizon and a target amount for each goal, and establish their risk profile for each investment. “Based on the client’s inputs, CONNECT generates a profile of the investor,” Charlie O’Flaherty, head of digital strategy and distribution at Crossbridge, told The Asian Banker. “CONNECT uses a ‘Certificate‘ structure, which offers diversified portfolios with exposure to up to 12 asset classes which are rebalanced regularly. We (also) know that a client’s capacity to bear risk can change as their life events do, so CONNECT embeds a suitability process into each goal that the client creates.”

While Crossbridge designed CONNECT to be intuitive so that investors can use it themselves, O’Flaherty said CONNECT was actually envisioned to be a hybrid model. “Clients may engage with us personally for more in-depth or custom solutions and advice,” he added.

While CONNECT is currently open only to accredited investors, O’Flaherty said a typical CONNECT client would be an unusually large client for retail banking, yet not quite wealthy enough to engage a private banker. “Through our CONNECT platform, these clients can benefit from the knowledge and experience we have gained through serving our ultra-high net worth client base. If we are able to provide value for clients, then in a short time I expect to see a significant increase in the amount of assets under management (AUM) shifting to the digital advisory model.”

A bright future

The outlook for robo-advisors, globally and in Asia, is clearly bright. BI Intelligence expects robo-advisors to manage $8 trillion globally by 2020, while McKinsey estimates the potential value to be around $13.5 trillion.

To compete effectively, multinational and local financial institutions as well as fintechs will need to move beyond simple engines to offer more sophisticated advice, customised solutions, dynamic rebalancing, and a multitude of other complex and high-value services. Customer demand is growing, the potential revenue is high, and industry players that lag behind may well see their customers shifting to other institutions that can use robo-advisors to power ahead.

All Comments