BNPL services started to gain popularity during the COVID-19 pandemic. Due to its accessibility and flexibility, customers can make purchases and spread the costs over monthly instalments. This solution was introduced to address the needs of digitally-savvy customers in various countries in Africa as a way to include unbanked populations in the region.

Fintech players are well-positioned as BNPL service providers. They are able to leverage technology and access behavioural and transactional data from mobile devices to assess prospective customers’ creditworthiness despite their lack of formal credit profiles or scores.

In light of the rising competition from fintechs offering BNPL services, banks risk losing customers to these alternative financing methods.

Consumers are increasingly adopting BNPL and pushing banks and other traditional payments providers to offer similar services. Instead of making payments instantly for an item or service, customers typically make the payment in three to six scheduled interest-free instalments. At the same time, vendors are embracing BNPL to attract new customers and enhance sales.

In South Africa, before the advent of BNPL, lay-by was the traditional way to pay for purchases in instalments. Instead of buy-now-pay-later, it was pay-now-buy-later. Customers would purchase an item with interest-free instalments, of not more than three months, and offer a minimum down-payment of 20%. The item will be held by the seller until the full amount is paid.

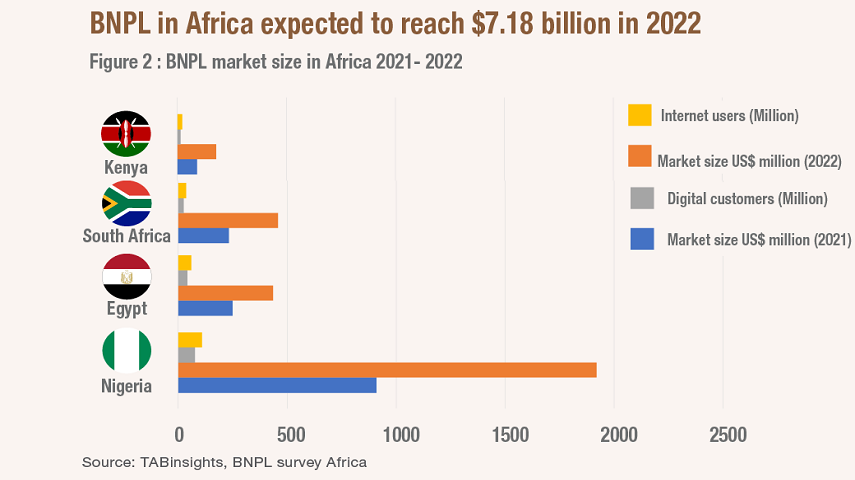

Payflex is one of the largest BNPL players in South Africa, with more than 1,000 merchants and 135,000 customers. Through their services, customers would pay only 25% of the purchase price and pay the rest over a few weeks at no additional cost. In April 2021, Australian BNPL company, Zip, acquired a 25% stake in Payflex

In Kenya, Lipa Later was launched in 2018. It is a BNPL platform that has expanded to various other markets in the region including Rwanda, Uganda, Ghana and Tanzania. It partners with retailers to allow shoppers to pay for items including furniture, electronics, and groceries in monthly instalments. One of these is Carrefour, the French retailer which has expanded its footprint significantly in Kenya, with 12 stores in Nairobi alone, 16 in total countrywide as of 2021.

Meanwhile, new BNPL fintech players were launched in Morocco and Egypt. Sympl, an Egyptian fintech, targets around 50 million debit and credit cardholders in the country. The company has raised $6 million in funding since its launch in October 2021. In Morocco, Chari, a business-to-business (B2B) e-commerce platform is testing BNPL services with customers with the goal of acquiring a local consumer credit company. Chari will enable shop owners to lend money to their end-users and further grow their businesses.

Banks may need to rethink their positioning in the market given the growing interest from both customers and merchants for these services. With the increase in the number of BNPL players, partnerships between banks and such fintechs would enable the former to expand into new innovative credit options while providing capital to the latter. On the other hand, banks can provide proprietary offerings by developing their own platforms, and investing in such payment infrastructures. Banks can also expand their credit card offerings to include BNPL services.

Amid the fast growth of the BNPL market, regulators are concerned about rising indebtedness and risk to consumers. BNPL providers can help mitigate these risks by improving their monitoring and understanding of customers' financial and transaction history and behaviour to have more accurate and secure credit risk assessment.

All Comments